We will provide Article to present the “ BTCCREDIT p2p lending” project to potential platform participants and those who are interested in contributing to its development. The information listed below may not be complete and does not imply any contractual relationship. The main purpose is to provide information to everyone, so that they can determine whether they are willing to analyze the company with the intention of obtaining token or invest.

Blockchain is making history by shifting power from centralized entities into the hands of the consumers. It has empowered people to manage their own assets without the intervention of any banks, brokers, or institutional monitors. This is a welcome necessity since people risk too much today by allowing their crypto assets to be controlled by a central entity. They don’t realize that it is not them but Wallets, Exchanges, & Lending Platforms that are controlling their assets. Hence, they have given up control of their identity, privacy, and money because they believe that they don’t have a choice. But not anymore.

The hope of joining the This project is very big for us, before you join it will be better if you understand the project besides it will add to your insight and improve information for you especially understanding the project’s vision and mission so that it adds to your trust in.

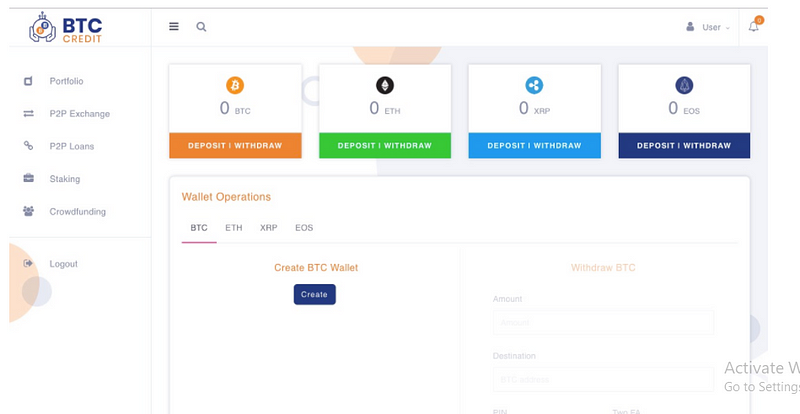

BtcCredit is an all-in-one decentralized wallet which gives you complete control of your Blockchain asset to Hold, Exchange, Lend, Borrow, Invest, and Stake. This document outlines the design of a Decentralized Next-Gen Banking Ecosystem that is powered by decentralised multi-currency wallet, decentralised p2p lending, and decentralised p2p Exchange capabilitie.

Video Introduction :

Fixing the Lending Market

Today the inflation-adjusted interest rate in different countries varies based on the available liquidity. In high liquidity market, Europe, interest rates are between 0.5–5 %, in Russia 12–15 %, in India 12 % and in Brazil 32 %. This shows a clear inequality in the way access to the lending market is distributed across the world. We believe that this inequality between the borrowers should be flattened and huge market value can be created in the process, especially through opportunities of Arbitrage. Banks charge 5–12% interest on loans and compensate you 0–1% for holding your assets with them. With the rise of crypto-currencies and Blockchain, you can now become your own banking institution. BtcCredit makes this a reality for you. Not just this, you decide whom you want to lend your money to, on which interest rate, and it what mode. All of this is available thanks to Blockchain technology, on which the Wallet of BtcCredit relies on.

Traditional P2P-Lending

Traditional P2P lending is similar to institutional lending, where some measure of credit history and creditworthiness of the borrower is taken into account. The creditworthiness of the borrower decides the type of loan deal he/she is offered.

The method to calculate the risk/credit score is managed through proprietary algorithms/artificial intelligence. The differentiation is also maintained through how defaults are handled, and penalties are imposed.

Crypto P2P-Lending

There are some existing Crypto lending platforms which are following different business models. On one end they are a just like a traditional p2p lending platform with the ability to accept cryptocurrencies as collaterals. On the other end, they deploy the entire loan contract on the blockchain and execute events on the loan agreement through smart contracts.

The blockchain technology, with its fully transparent and incorruptible transaction ledger, forms the ideal system for managing the loan with its parameters like tenure, interest rate, crypto collateral, etc.

There are many platforms that offer crypto lending:

● Sofin

● Everex

● Ethlend

● Lendoit

● Btcpop

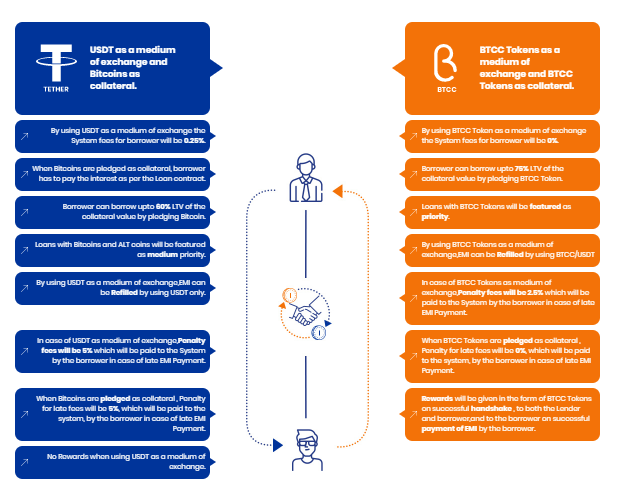

Medium exchange

Exchange as collateral and USD as a medium of Bitcoins.

How the System will Function

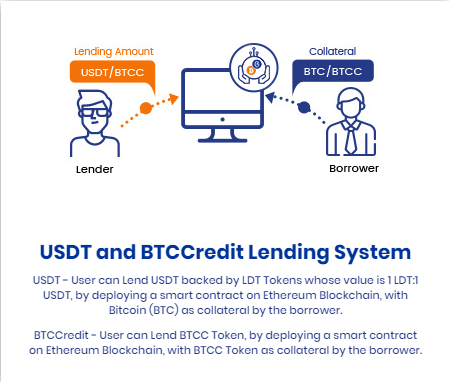

The LDT Token The system will use an intervening ERC 20 token to manage the repayment through token offset. The token will follow the loaned amount into the wallet of the borrower and will be returned as the borrower repays the instalments.

The Lender’s Pride The Lender’s Pride platform proposes to enable a loan marketplace with some unique features. The system being proposed will form a forum for lenders and borrowers to check loan and loan request offerings including the loan parameters being offered. Based on their own risk perception ability to repay interest, the lenders and borrowers will “handshake” with each other to create a loan agreement on the blockchain

How Does it Work?

As a lender, a user enters the system and funds his system generated Wallet with USDTs. The system creates a lending profile where his acceptable loan parameters are recorded. The lender’s loan profile becomes a part of a “credit marketplace”. As a borrower, the user enters the system with his system generated Bitcoin wallet. The bitcoin funds in the wallet form the collateral against the potential loan. The borrowing requirement also becomes a part of the “credit marketplace”. A system internal logic automatically matches and suggests existing loans and borrowers. A borrower or lender can also manually select from a set of loan offerings or borrower’s requirements.

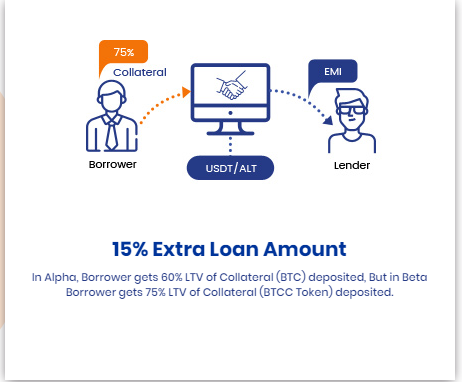

Once a loan is selected, and both sides agree to the parameters on the book, a “handshake” is said to have taken place, which will result in a deployment of a smart contract on the Ethereum network. The borrower’s wallet will be funded with the requested USDT and a schedule for repayment gets created.

The repayment is recorded as the borrower deposits the instalment of USDT back into his WSDT wallet. A set of terms and conditions kick in in case the payment is delayed, is not enough or is more than required instalment.

In this digital age, users have unlimited number of options to choose from, so unlike last time when banks never used to focus on customer experience, will have to pivot their strategy. http://btccredit.io

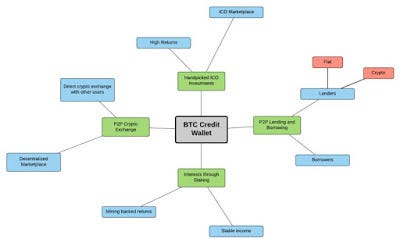

Defining the BTC Credit Platform Keeping the competitors in mind and analyzing the market conditions and trends, BTC Credit has been able to identify 4 key verticals when it comes to the services offered by its Wallet:

1. P2P Lending and Borrowing

2. P2P Crypto Exchange

3. Handpicked ICO Investments

4. Interests through Staking

All of these services will be offered with the help of a Wallet on the platform. Think of the platform as a Bank and the Wallet as a Bank Account. Analogous to the Banking System today, the user can load the Wallet with fiat or cryptocurrencies and use the funds to avail services in all the 4 verticals mentioned above.

Repayment Conditions

When the Contract is completed or in case of foreclosure the borrower’s request for the return of their collateral of BTC deposited they can raise a request for BTC withdrawal and it can be completed.

Normal repayments — The Admin Pays the Lender instalment regularly and the Borrower pays the Admin Regularly, the system will be notified by the blockchain of the next instalment date of the Borrower.

Instalment Delayed — If the Borrower Missed the date to Pay the instalment the API Interface will notify the Front-end of the Missing instalment of the Borrower. The borrower gets 3 days of grace period to pay the instalment. if the instalment is paid within 3 days no fine will be charged.

Instalment Delayed and Missed — If the Borrower missed the date of instalment he will be given 3 days of a grace period and even he misses to pay the Borrower will be fined for the particular instalment.

Borrower Defaulter — If the Borrower is unable to pay 3 consecutive instalments the system will be notified by the blockchain as the Borrower is Defaulter and the Front end can Confiscate its collateral.

Pre Closure Loan — If the borrower wants to Pre Close the contract he can close the Contract by paying the Principle + 5% Interest and close the contract but he can do only if he has paid 3 consecutive instalments

Extra instalment Payment — Here the instalment Amount is 1010 Every 30 Days, assuming the user deposits 1500 USDT/LTD and he is willing to pay more than the instalment Amount he can do it, but the next monthly instalment amount doesn’t change its kind of foreclosure that meant the extra amount will be deducted from the last instalment, so if the amount is greater than the Last instalment then it will consider the Second Last and So on, if the Extra amount is greater than Last 3 instalment he has to either Pre close the entire contract or he can lower the Tenure till 3 instalment.

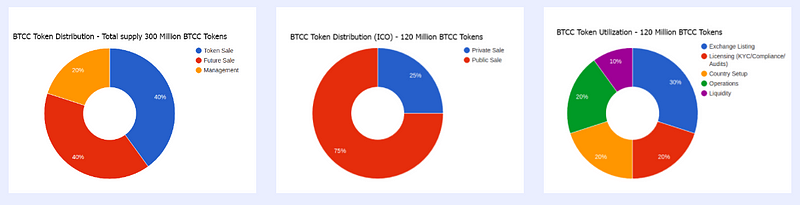

Token Distribution

For More Information You Can Visit Link Below :

WEBSITE : http://btccredit.io/

FACEBOOK : https://www.facebook.com/btcctoken/

TWITTER : https://twitter.com/btc_credit

MEDIUM : https://medium.com/@info_60688

INSTAGRAM : https://www.instagram.com/btccredit/

WHITEPAPER : http://btccredit.io/pdf/btccredit_whitepaper.pdf

AUTHORS : Letty sits

BITCOINTALK’S PROFILE : https://bitcointalk.org/index.php?action=profile;u=1898514

Tidak ada komentar:

Posting Komentar